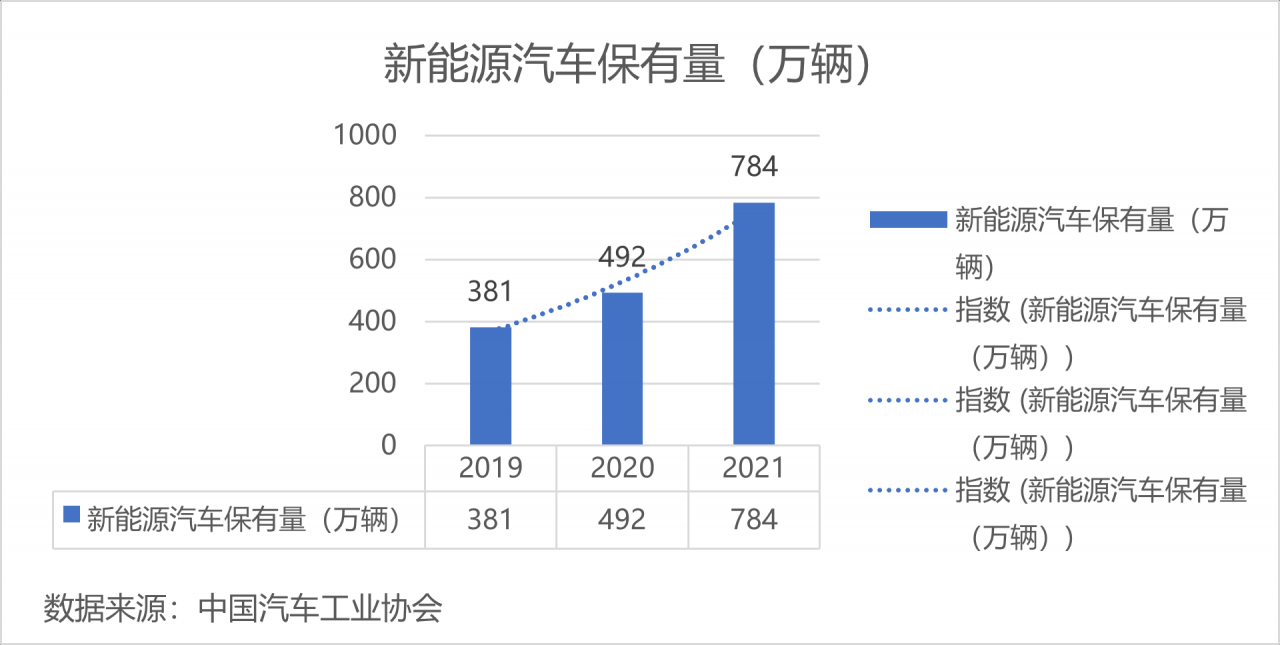

this summer, the world ushered in high temperature scorching, and the consensus among governments to prevent global warming has experienced another wave of strengthening. in terms of the automobile industry and the new energy industry, it adds another fuel to the trend of abandoning oil and switching to electricity, which is already in full swing around the world. according to statistics, the number of new energy vehicles in china has exceeded 10.01 million this year, and only in the first half of 2022 as of the end of june, the number of newly registered new energy vehicles in the first half of the year has reached 2.209 million, which is the same as that in the first half of 2021. compared with an increase of 1.106 million vehicles. the growth rate of the number of new energy vehicles from 2019 to the end of 2021 reached 105.8%.

new energy vehicles have such a momentum, new energy batteries are the heart of new energy vehicles, the demand is increasing steadily, and the upstream raw materials of power batteries are also rising. at present, there are five types of batteries used in new energy vehicles on the market, namely:lithium cobalt oxide battery, lithium iron phosphate battery, nickel metal hydride battery, ternary lithium battery, graphene battery.

these five types of batteries have their own advantages and disadvantages. among them, the technology of lithium cobalt oxide battery is the most mature, but at high temperature, its stability is not as good as that of lithium iron phosphate battery. although the lithium iron phosphate battery is unique in terms of stability, its energy density is not as good as other batteries, and the charging efficiency will decrease in an environment below minus five degrees. in cold regions such as northeast china, it may even affect the service life of the battery. as the only product among the five types of batteries that does not belong to lithium batteries, nickel-hydrogen batteries have the same disadvantages as graphene batteries. they perform very well in all tests, but the cost is too high. at present, the most suitable for the development direction of new energy vehicles in the future is the ternary lithium battery, which has high safety and stable voltage.

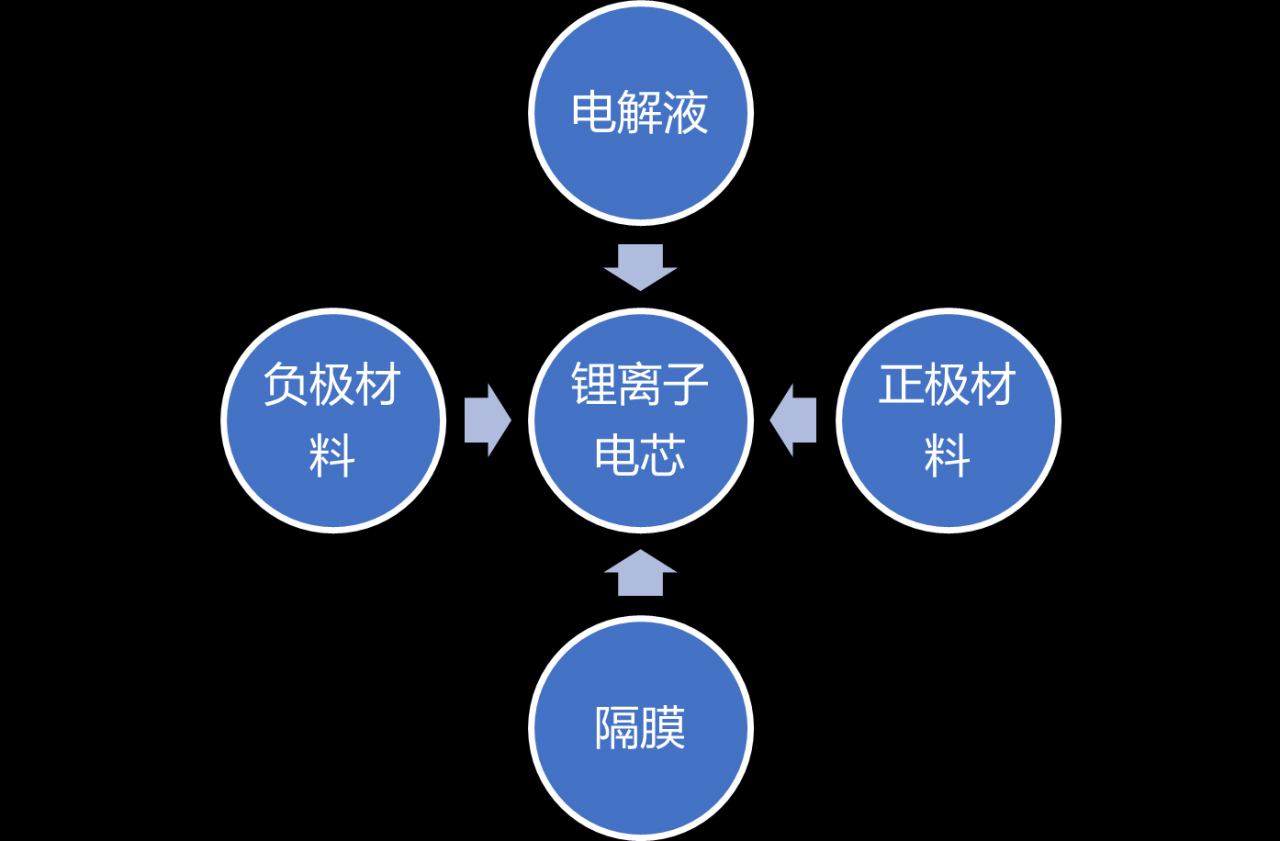

among the five types of batteries, the four types of batteries other than nickel-metal hydride batteries have similar requirements for upstream raw materials in terms of types and quantities. the main upstream raw materials of the four batteries can be divided into positive electrode materials, negative electrode materials, electrolytes and separators. lithium-ion batteries can only be produced by processing four materials.

as shown below:

if lithium-ion batteries are the heart of new energy vehicles, then lithium-ion batteries are the heart of lithium-ion batteries. the electrolyte is the most important blood in the production of the battery, and the solvent is indispensable for the production of the electrolyte.

currently the actual consumption of lithium battery electrolyte solvent accounts for about 60%~70%, of which lithium salt accounts for about 8%, and additives are between 5%~10%. dmc, the nstream product of po, is an important part of the electrolyte supply chain. it has the advantages of low odor, strong solubility, high effect on improving the conductivity of lithium batteries, and low cost. it is currently the most widely used organic solvent in electrolytes. . and both emc and dec solvents can be synthesized from dmc. since 2019, the nstream market structure of dmc has changed, and the electrolyte solvent has become the main new consumption terminal of dmc. under such a market prospect, coal chemical industry lines such as hualu hengsheng also want to take advantage of the company’s own cost advantages, and have carried out the 300,000-ton dmc projectput into production. however, companies such as shida shenghua, which has a relatively complete system for the electrolyte solvent industry chain, claim that the coal chemical route can only achieve emc, dec, and dmc. the key ec and pc solvents must come from the petrochemical industry. the shortcomings that cannot be made up by the chemical route. and the most important thing is that, according to the rules of mainstream electrolyte manufacturers, most of them purchase five kinds of solvents from the same supplier, in order to ensure the quality of the final electrolyte in the safest way.

it is expected that 1.8 million tons of new dmc capacity will enter in the next 3 years. in the dmc industry, there will continue to be a cross game between the coal chemical industry with the advantage of low cost and the petrochemical industry of the whole industry chain of electrolyte. the near halving of the electrolyte in 2022 is the best proof, and the low-cost coal chemical industry may indeed pose a big threat to traditional petrochemical companies by competing for production capacity and output in the short term by virtue of its price advantage. however, the technological advantages of petrochemical companies in the entire industry chain are also long-term high ground that coal chemical companies cannot occupy. the large-scale rise of new energy vehicles has led to the enthusiasm for the lithium mining industry and lithium batteries, and then to the cost and price competition in the electrolyte solvent market. the interlocking links will also drive the new pattern of the entire po nstream market. at present, the main nstream industry consumption of po is still 77.2% of polyether polyols. in 2021, the consumption of dmc will be 9.0%, ranking second, a decrease of 0.6% compared with the same period in 2020. even so, the dmc consumption of the petrochemical route is showing an upward trend. it is believed that the future lies in the continued steady growth of the petrochemical dmc market after the price war among coal chemical companies.