propylene oxide

10 the nstream performance of propylene oxide was relatively flat, and the overall chemical market was not prosperous. end-customer market is mediocre. after the 11th national day holiday was stabilized, the propylene oxide market benefited from replenishment on the demand side and individual fluctuations on the supply side. the market price in shandong quickly rose from 9,500 yuan/ton to 10,200 yuan/ton, but the upward trend fell rapidly. the follow-up on the demand side is becoming weak, coupled with the partial recovery of the load reduction and maintenance equipment on the supply side, and the successful start-up of taixing yida’s annual production of 150,000 tons of propylene oxide plant, the market supply is still abundant, and it is difficult to find good support and the market is difficult maintained a high level of more than 10,000 yuan, and in the middle of the month, cyclopropane manufacturers stabilized the market at 10,200-10,300 yuan/ton and then began to fall.

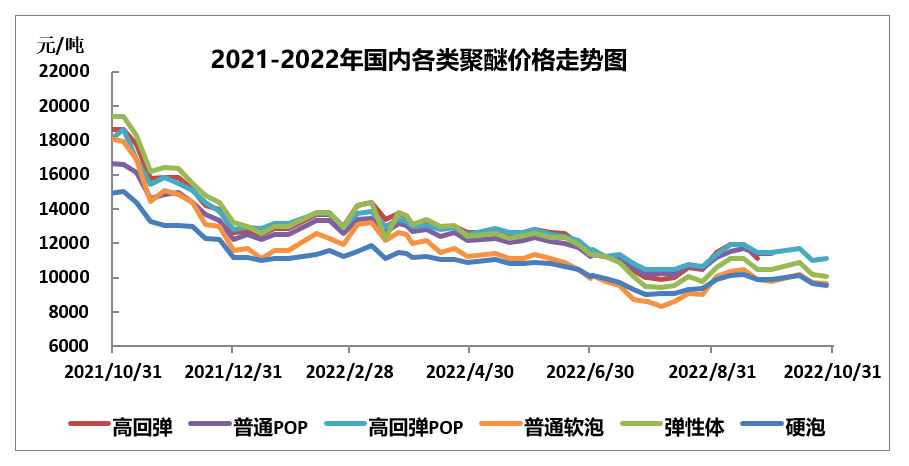

polyether polyol

as the traditional peak season of “silver ten”, the overall nstream demand in the polyether market remains light. nstream of soft foam: although some nstream orders such as automobiles and upholstered furniture are not as expected, they have increased slightly, and the demand for stocking has also increased slightly. nstream of hard foam: the demand for raw materials from the home appliance industry is slightly better than in september, mainly due to the rebound in domestic sales. however, the recent ice-cooled production still shows a year-on-year decline, which is mainly dragged n by the decline in cold export business. in the first half of october, the demand for cold storage panels, spraying and pipeline engineering remained relatively active. in the second half of october, with the completion of outdoor insulation projects in the north, the demand for raw materials declined. on the other hand, the worsening epidemic situation in many places in the second half of the month has also caused some nstream manufacturers to reduce or stop production. affected by seasonal factors, the consumption of hard foam nstream pipes, spraying, and exterior wall industries has dropped significantly; the demand for home appliances has generally followed up. during the month, multiple sets of tdi plants in europe were shut n, and the operating rate of domestic plants was only maintained at about 30% at the lowest point. due to the impact of the epidemic in xinjiang, transportation was blocked, and tdi’s main factories all shipped in limited quantities. the overall spot market continued to tighten, prompting tdi the market price has risen sharply, and the price has been hyped to 26,000-26,500 yuan/ton (domestic products), which is 5,500-6,000 yuan/ton higher than before. high prices suppressed the industry’s enthusiasm for polyether trading, and the overall polyether trend fluctuated around the weakness of cyclopropane.

forecast:

supplysupplier: binhua11month11overhaul from day10outside of the sky, the polyether plant maintained a low load due to the loss of some grades.

cost end: jiangsu yidapodevice11restart in the middle of the month; tianjin sanpec and qixiang tengda are expected to put into production, sinochem quanzhou, zhenhai phase ii, jinling, and tianjin bohua plant maintenance7current load; daze restarted recently; binhua cyclopropane has reduced its load until the end of the year, and the supply pressure of cyclopropane is high.

demand side: the real estate market is unlikely to improve significantly in the short term, and the recovery of the new housing market in some cities still faces greater challenges under pressure, the national real estate market as a whole maintained a bottoming market, and urban differentiation intensified. the epidemic situation in some areas is spreading, and the prevention and control efforts are intensified. the polyurethane terminal industry continues its off-season, and the market demand is expected to turn weak.

in summary:11monthly polyether polyols continue to be weak.